Attention

Bloomberg.

and

-

Cash bonds shrug off withdrawals, stumping strategists

-

Fund flows act as barometer for broader fixed-income, stocks

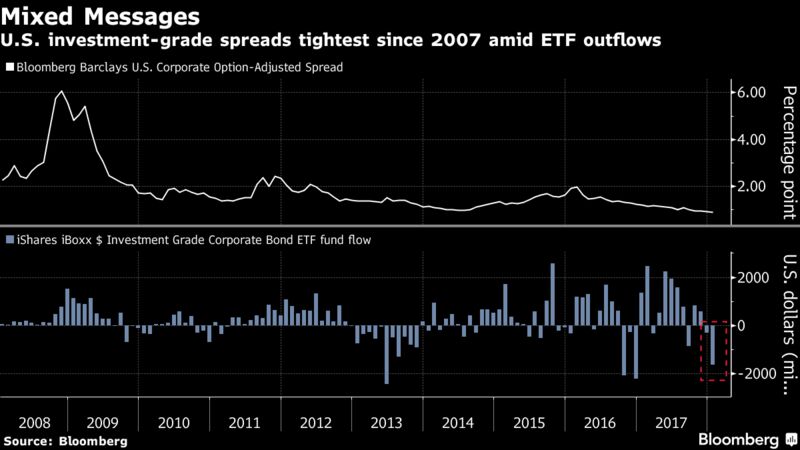

U.S. corporate debt exchange-traded funds have bled a near-historic sum of assets over the past two weeks, but holders of the underlying securities are paying little heed.

The bonds themselves are enjoying some of the tightest spreads on record as appetite for new issues remains strong. On one hand, tax reform, rising oil and global growth may be fueling demand for yield. Yet the ETFs — in the midst of the longest outflow streak in at least seven years — point to a downturn.

The divergence is stumping Wall Street strategists who use the ETF market not only as a proxy for investor sentiment in debt, but also as a gauge of risk appetite for equities and other assets. Though technical quirks associated with ETF trading may have caused the dislocation, some analysts point to a simpler distinction: so-called dumb money versus smart.

“The tax package is probably giving institutional investors more confidence about the shape of corporate balance sheets,” said Matt Maley, a strategist at trading firm Miller Tabak + Co. “Thus they might be making up for the selling that is coming from these products geared towards individuals, who are worried about the rise in government yields.”

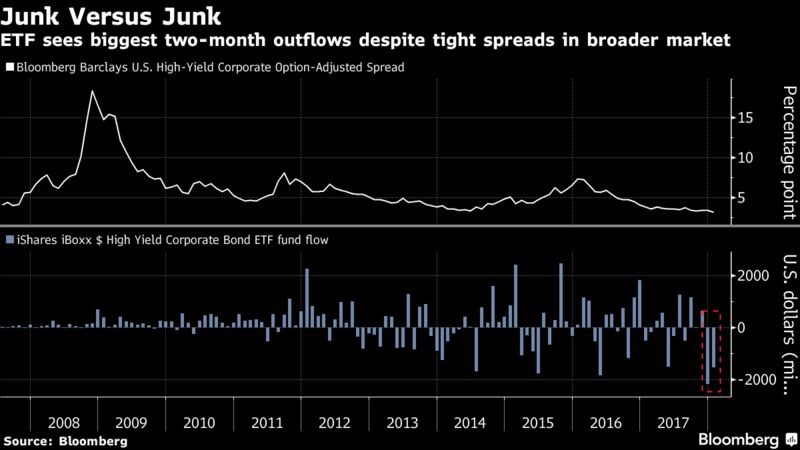

U.S.-listed corporate bond ETFs are headed for a second consecutive month of outflows, the first time that’s occurred in at least seven years. The pain is across ratings. The iShares iBoxx Investment Grade Corporate Bond ETF, LQD, had the biggest day of losses last week since 2016, while BlackRock’s high-yield equivalent, HYG, is in the midst of its biggest two-month outflows on record.

If the withdrawals are a symptom that retail funds are losing their taste for fixed-income, the impact could be far-reaching. A tweet from DoubleLine Capital LP co-founder Jeffrey Gundlach Thursday — who has previously warned underperformance may portend a selloff for risk assets — noted the gap between junk ETF prices and stock gains.

Strategists at JPMorgan Chase & Co. expect individual investors to be the « wildcard » for bond markets grappling with diminished central-bank stimulus, while dollar weakness may curtail foreign inflows to U.S. corporate bonds.

Spreads in junk and investment-grade bonds sit near the tightest since 2007 even after high-yields premiums rose slightly. Meanwhile, investors pulled more than $1.9 billion from U.S.-listed corporate bond ETFs in the week to Jan. 19, the second consecutive five-day period of outflows.

ETF constituents can differ from benchmarks due to liquidity and other portfolio constraints, so some technical factors may be at play. LQD, for example, has greater sensitivity to interest-rate risk, with a modified duration of 8.7 years, compared with 7.6 years for the broader Bloomberg Barclays U.S. Investment Grade index.

« It looks like constituents — either maturity, credit or liquidity differences between the two markets — have played a role, but there does seem to be a general weakening of ETFs relative to the market, » said Thomas Tzitzouris, fixed-income research chief at Strategas Research Partners. « At a high level, we believe that high-yield is running into resistance. »

What’s more, ETFs typically serve as « placeholder » vehicles in lieu of strategic allocations. Investors, therefore, may be putting cash into work in the primary market during the January deluge at the expense of passive instruments.

It’s much faster to make a short, or bearish, bet on an ETF than through cash bonds, according to Andrew Brenner, the head of international fixed-income at Natalliance Securities in New York. Later when traders cover those shorts the ETFs recover, he said.

“The actual bonds could take a week to move while the ETF takes 10 minutes, » he said. « But we have seen this before and the market has held, and then shorts have to grab the ETF so it outperforms. »

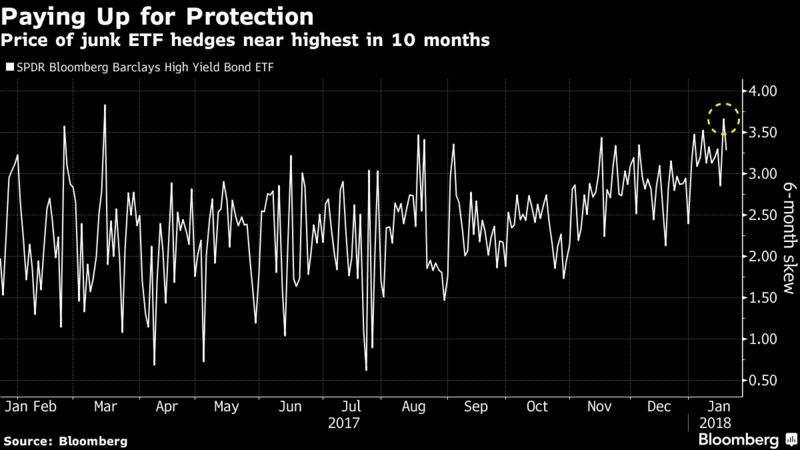

In the short-term, the swelling gap between ETFs and the underlying market may expose some investors to basis risk, or the peril of hedging bond exposures through passive investments.

“At the very least ‘credit hedge’ products are underperforming,” Peter Tchir, the head of macro strategy at Academy Securities Inc., wrote in a note Friday. “Whether a precursor to wider weakness or setting the stage for one gap tighter back to levels closer to pre-crisis levels is the big question. With the year off to such a great start, I would err to the side of caution here. ”