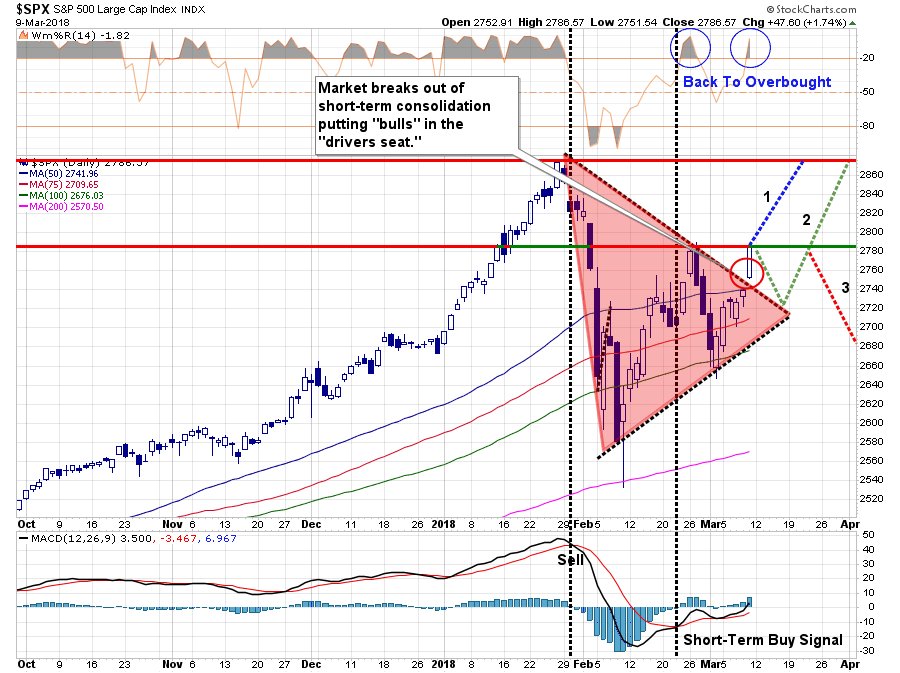

Notre proxy du marché mondial, le S&P 500 est sorti par le haut

Divergences franco-allemande sur la réforme de l’Europe

Les Français veulent que les Allemands acceptent de partager les risques , mais les Allemands exigent qu’il n’y ait plus de risques.. avant de les partager! La discipline doit précéder la solidarité. Et puis il y a l’Italie!

The expectations could not have been higher. After the election of Emmanuel Macron in France, there was hope that the euro zone could finally press ahead with an overhaul of its economic governance, which would make it more resilient in a crisis.

The contours of the planned deal were very clear: fiscally conservative countries, such as Germany, would agree to greater « risk-sharing, » for example setting up a joint scheme to guarantee deposits or a “rainy day” fund to help countries facing a shock. Meanwhile, vulnerable states such as Italy or Portugal would agree to reduce risks in the balance sheets of banks and in the public finances.

The missing piece was a government in Germany. It took nearly six months for Angela Merkel’s Christian Democratic Union (and its sister party, the Christian Social Union) to form a grand coalition with the Social Democratic Party. A vote by the SPD a week ago cleared the last obstacle. The « Franco-German engine, » as it is often called, looked ready to lead Europe once again.

The differences have been clear for weeks. Germany would like banks to reduce the amount of government debt on their balance sheets to prevent a sovereign crisis turning into a banking crisis. Berlin is also keen on a mechanism to make it easier to restructure sovereign debt when a country asks for help from the European Stability Mechanism, the euro zone’s rescue fund. So far, Bruno Le Maire, France’s Finance Minister, has soundly rejected both ideas.

It is also unclear how enthusiastic other member states really are about such a bargain. Last week, eight northern states including Finland, Ireland and the Netherlands, said that greater fiscal discipline and more progress on structural reform at home should come before any far-reaching proposal. While they remain committed to the completion of a “banking union,” they looked reluctant to embark on more ambitious projects.

“Stronger performance on national structural and fiscal policies in line with common rules, along with these European initiatives, notably the banking union, should have priority over far-reaching proposals,” they wrote in a joint document.

Finally, there is Italy, the giant elephant in the room. In the general election on Sunday, anti-establishment parties such as the League and the Five Star Movement won 50 per cent of the vote, with platforms that contained lavish pledges (including a flat tax for the League, and a « citizen’s income » for Five Star) that are clearly incompatible with the euro zone’s fiscal rules. Neither party was able to secure a majority and, for now, there is no sign they are willing to form a « populist » alliance. Still, their success is a clear sign that Italian voters are reluctant to be subject to greater fiscal discipline.

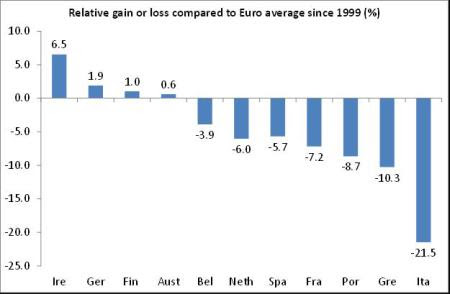

Le mythe de la convergence qui est à la base de la volonté de réforme de la Construction Européenne explique les réticences allemandes. La construction européenne exploite les italiens, pompe leur valeur et leurs richesses sont transférées à l’extérieur; et au lieu de converger on diverge encore plus. Même remarque pour la France mais à un degré moindre

Italy’s vote is a reminder to countries such as Germany that they cannot count on having fiscally prudent governments across the euro zone. Once they sign up for more risk-sharing, such mechanisms could be abused, unless proper checks and balances are in place. This will make Berlin more skeptical of euro-zone reform.

While European leaders will meet in two weeks to discuss a range of subjects linked to the future set up of the euro zone, the real tes will be in June, when they are expected to take more concrete steps. In particular, two areas will show whether the euro zone is willing to make real progress: The first, is whether leaders agree to strengthen the « single resolution fund, » a common pot of money which is used to restructure banks in trouble, for example by letting it have a credit line to the ESM. This would ensure the fund has enough money to handle large banking crises.

The second area is progress on a joint deposit insurance scheme. Of course, it would be unrealistic to believe that countries can mutualize their safety nets immediately. But it is necessary to take some initial steps, which would ensure, for example, that national schemes insure each other in the event one of them cannot come with a shock. The only way that will be politically acceptable is to continue to reduce risks present in the balance sheets of banks, in particular speeding up the reduction of non-performing loans.

These moves now look harder than they once seemed. But they remain essential for the euro zone to thrive. For all their mutual differences and the skepticism of their partners, Germany and France should not abandon their ambition.

[Bloomberg] Stocks in Asia Rally After U.S. Jobs; Yen Advances: Markets Wrap

[Bloomberg] Emerging-Market Investors Face a Week of Tumult as Trade War Looms

[Bloomberg] London House Prices Are Dropping at the Fastest Pace Since 2009

[Reuters] Japan PM, finance minister face mounting pressure over suspected cronyism scandal

[WSJ] U.S. Trading Partners Seek Guidance on How to Avoid Tariffs

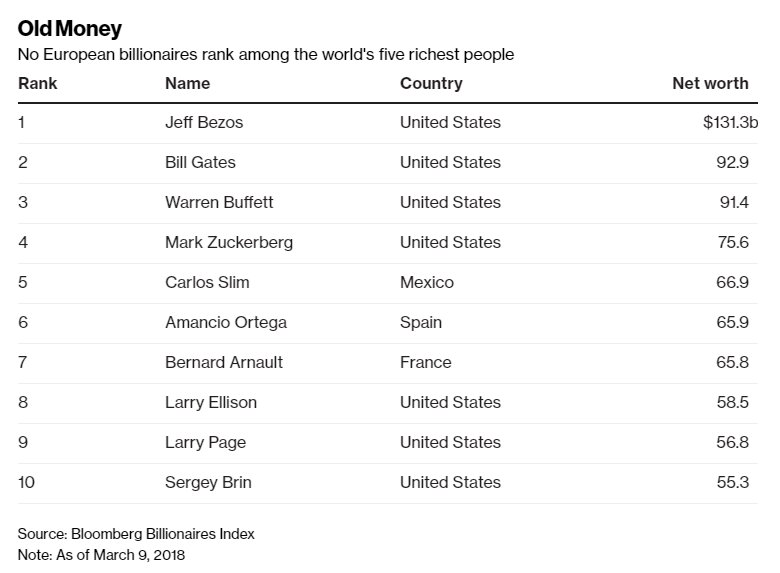

Les milliardaires.