La Fed refuse d’etre préemptive , il faut dire qu’en 2018 quand elle a essayé de l »être, elle s’est prise une sacrée claque.

Elle attend donc la croissance et l’inflation sans se laisser influencer par les attentes.

Elle veut toucher pour croire.

L’intervention de Powell ce jour doit alimenter les anticipations d’inflation, la hausse des taux longs et l’euphorie boursière.

Attendons la suite.

Nordea Bank

The Fed is now officially behind the curve and Jay Powell is even proud of it, but he made a potentially costly mistake by admitting to having to quantify what a moderately overshooting inflation rate means as soon as inflation overshoots the target.

The Fed sounded more upbeat on economic projections but also kept referring to the fact that they want to see actual progress and not forecasted progress before changing anything in the policy framework.

Powell made a mistake by admitting to having to quantify what a moderately overshooting inflation rate means as soon as inflation actually overshoots target. This clearly raises the stakes markedly ahead of Q2.

The risk of a taper tantrum 2.0 remains high in April/May.

Key take-aways from the FOMC-meeting

- A message on SLR will arrive in the coming days.

- The Fed keeps repeating that inflation will be allowed to overshoot and that they need to see the inflation first before anything related to tightening can be just barely considered

- The Fed needs to see actual progress and not forecasted progress

- This will, in our view, allow USD bond yields and inflation expectations to continue to increase during Q2 (potentially a lot)

The main take-aways from the statement and economic projections

The Fed is clearly more upbeat on growth than in December for good reasons, but they still want to send a signal that inflation will be allowed to overshoot target without an immediate tightening response.

They expect core PCE prices at 2.2% for this year and 2.1% in the endpoint in 2023.

Four out of eighteen FOMC members see a rate hike in 2022 compared to only one in December, which is another way of showing that the Fed has turned more upbeat, but they remain extremely cautious in terms of sounding just barely tightening biased and a clear consensus still refrains from hinting of any hikes at all.

None of this came as a surprise to markets, even if markets had slowly but surely built up a tad of hawkish expectations on forehand. Otherwise, the statement included almost exactly the same guidance as last time except for a slightly more upbeat tone on activity (GDP growth projections for 2021 lifted to 6.5% from 4.2% in Dec).

The immediate market reaction is accordingly slightly dovish.

The main take-aways from Jay Powells press conference

On SLR

Jay Powell firmly rejected the possibility to talk about the hot topic of the Supplementary Leverage Ratio and promised that the Fed would post something official on the topic in the “coming days”. We still consider a prolongation of the SLR-relief unlikely, but the Fed is likely to come up with more politically palatable mitigating action.

The small change to the counterparty limit on the overnight RRP facility to 80bn per day from 30bn earlier, may be a first sign of that.

On AIT and inflation pressures

Powell refrained from specifying what a moderate overshooting of the inflation target means, but kept saying that the Fed now purposely remains behind the curve as they “need to see actual progress, not forecasted progress.” … But he made a small and potentially costly mistake by admitting to having to quantify what a moderately overshooting inflation rate means as soon as inflation overshoots the target. Powell said that “..we have resisted the temptation to try and quantify what that means, but when we are above target… we can do that” .

This will leave stakes SUPER high ahead of inflation figures from April when the big inflationary effects start to kick in. After all, it is much easier to say that you will allow inflation to overshoot as long as you actually don’t overshoot, but once the overshooting kicks in, it will be much more difficult to sound as dovish.

Our main views compared to those of the FOMC

Below we try to compare our view on inflation, rates and the USD to those of the market and the Fed.

On inflation

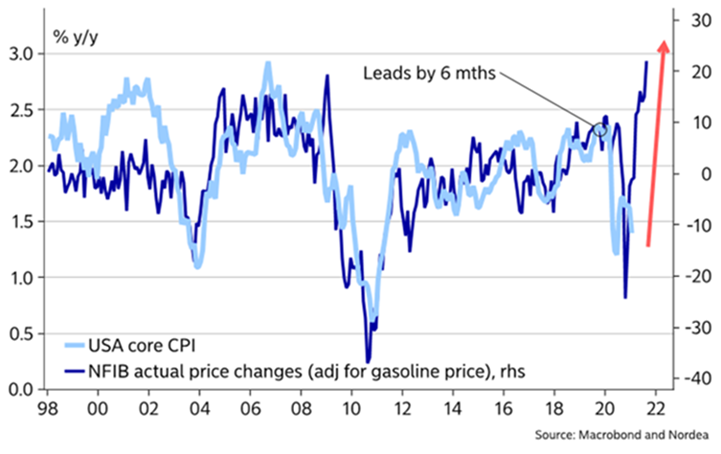

We remain very inflation bullish as the cocktail of widespread money printing and direct transfers is a potentially very inflationary cocktail, while companies are now also more price hawkish than we have seen in decades. Jay Powells commitment to quantifying what moderate overshooting means when overshooting happens will throw the Fed directly into this discussion in 1 or 2 months from now.

Chart 1. Inflation is coming!

On interest rates

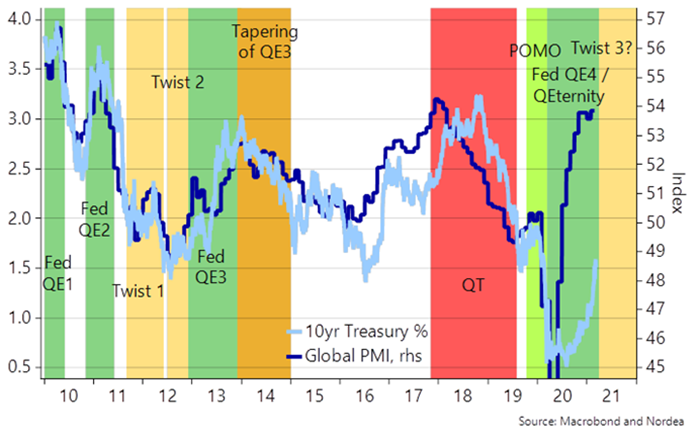

We remain in the camp of selling rallies in USD bonds and target 2% or above in the 10yr treasury yield over the coming 3-4 months. The Fed will face an uphill battle in containing long bond yields as the nominal growth momentum will put an upwards pressure on long bond yields almost no matter the Fed response. Increasing QE will likely rather just reflate long-term expectations even further and hence accelerate the current move in the long end of the yield curve. By committing to staying behind the curve (as Powell did tonight), the Fed will also allow long bond yields and inflation expectations to run hotter than currently.

Should the Fed decide to move towards a WAM of 10yrs in the SOMA portfolio again (Operation Twist), it could work to temporarily dampen the steepening pressure in the USD curve, but it may not work as well as in 2011-2012 as the business cycle is gaining momentum, which usually leads to higher bond yields, not lower. Mind the gap between the Global PMI and 10yr bond yields? We target 2% in the 10yr Treasury already towards summer and project a first rate hike in H2-2022.

Chart 2. The Fed will face an uphill battle fighting against higher bond yields due to the strong business cycle

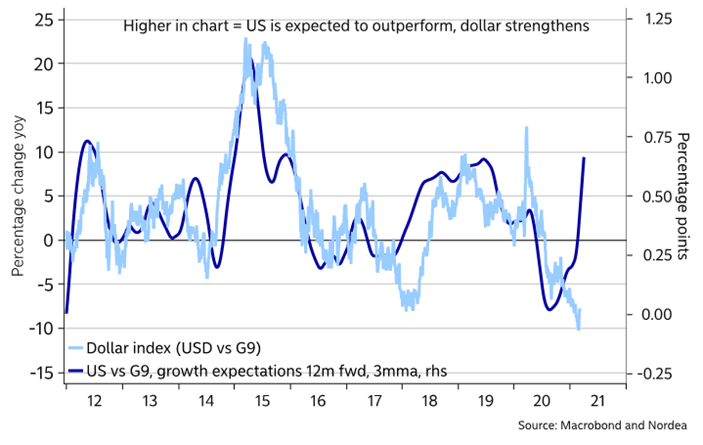

On the USD

Our view on USD interest rates could also lead to a reversal of the EUR/USD towards the second half of this year. We find it likely that we will end 2021 on clearly lower levels in EUR/USD compared to current spot, as the USD interest rates are simply more alive than EUR dittos, not least as the ECB seemingly wants to keep printing more into the economic rebound during the spring. The Fixed Income market also reflects relative growth perspectives, which simply look more upbeat in the US compared to in Europe, among other things due to a more successful vaccine roll-out.

We target 1.1750 in EURUSD over the next 2-3 months.

Chart 3. US growth expectations moving strongly to the USD’s advantage